T-Accounts Guide: Definition, Examples, Benefits, And How to Record

Tracking payables doesn’t have to be complicated. T-accounts, combined with accounts payable software, can transform how businesses manage invoices and payments, automate workflows and reduce errors. In this guide, we’ll discover what T-accounts are, how to record them, their benefits, and drawbacks.

Definition of a T-Account Explained

A T-account is a financial record of an account’s transactions, shaped like the letter “T.” The account name goes at the top, with debits on the left and credits on the right. It follows the principles of double-entry bookkeeping, where every transaction affects two accounts to maintain the accounting equation in balance.

How to Record the T-Accounts

To record a T-account, identify the accounts affected by the transaction (at least two), as double-entry bookkeeping requires at least two accounts to be involved in the transaction. Next, assign debits and credits: assets and expenses increase with debits, while liabilities, equity, and revenue increase with credits. Finally, subtract the smaller side (debit or credit) from the larger to find the balance.

Example: A $5,000 cash sale debits the cash T-account $5,000 and credits the service revenue T-account $5,000.

Problems With T-Accounts Recording

Recording transactions in T-accounts isn’t flawless. One issue is human error. Manually entering debits and credits can lead to misclassifying a transaction or entering the incorrect amount. As a result, accounting may end in discrepancies in financial statements.

Another problem is scalability. T-accounts are well-suited for small businesses or simple transactions, but they can become cumbersome for companies with high transaction volumes. Tracking hundreds of transactions across multiple accounts manually is time-consuming and prone to oversight.

T-accounts also lack context. They display debits and credits but don’t provide details such as transaction dates, descriptions, or supporting documents. As a result, these calculations are less useful for audits or detailed financial analyses without additional records.

Finally, T-accounts don’t integrate well with modern accounting software. Most platforms automate ledger entries, rendering manual T-accounts obsolete for large-scale operations. Still, they remain valuable for teaching, small businesses, or quick analyses.

Types of T-Accounts

T-accounts handle different transaction types based on account categories:

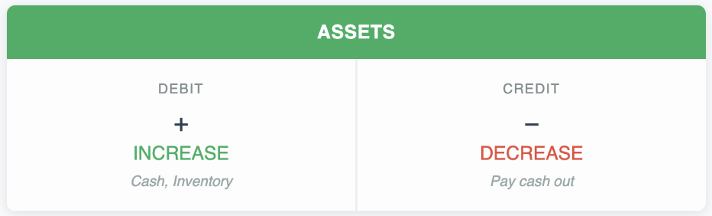

- Assets: Track cash, inventory, or accounts receivable. Debits increase these; credits decrease them.

- Liabilities: Cover accounts payable or loans. Credits increase them; debits reduce them.

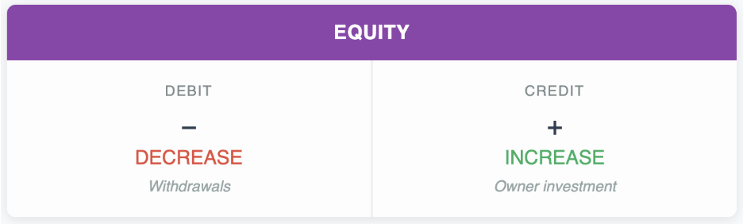

- Equity: Include owner’s capital or retained earnings. Credits boost equity; debits, such as withdrawals, lower it.

- Revenue: Record sales or service income. Credits increase revenue; debits, such as refunds, reduce it.

- Expenses: Track costs like rent or wages. Debits increase expenses; credits reduce them.

Each type follows the same T-Account structure but serves a unique role in tracking financial activity. For example, a cash T-account tracks money inflows and outflows, while a revenue T-account monitors income from sales.

Key Advantages of Using T-Accounts

T-Accounts shine for their simplicity and clarity. They make it easy to visualize how transactions affect accounts, which is especially helpful for beginners learning double-entry bookkeeping. T-accounts are quick to set up, requiring just a pen and paper or a simple spreadsheet.

They also help catch errors. Since debits must equal credits, imbalances are easily spotted. T-accounts are flexible and suitable for both small businesses and complex corporate ledgers.

After all, for small operations without access to pricey software, T-Accounts offer a cost-effective way to maintain accurate records.

Drawbacks of T-Accounts

Despite their benefits, T-accounts have limitations:

- Manual Process: Recording T-accounts by hand is time-consuming and prone to human error, especially for large businesses.

- Limited Scope: T-accounts focus on individual accounts, lacking the comprehensive view provided by financial statements.

- Informal Records: These are not formal tools and are not suitable for external reporting or audits.

- Scalability Issues: For businesses with high transaction volumes, T-accounts become impractical compared to automated accounting software.

These drawbacks highlight why T-accounts are often a stepping stone to more formal accounting records.

T-Accounts vs. Traditional Accounting Records

T-accounts differ from other accounting records in purpose and structure. Let’s compare them to standard accounting tools.

T-account vs. Journal Entry

Journal entries are the first step in recording transactions, they capture the date, accounts affected, amounts, and descriptions of the transactions. T-accounts are the next step, organizing those journal entries into specific accounts.

For example, a journal entry might record a $2,000 sale with a debit to Accounts Receivable and a credit to Revenue. The T-accounts for those two accounts would then reflect those amounts in their respective debit and credit columns. Journal entries provide the “what” and “when,” while T-accounts show the “where” and “how.”

T-Account vs. Balance Sheet

A balance sheet summarizes a company’s financial position at a point in time, detailing assets, liabilities, and equity. T-accounts, however, focus on individual account transactions.

For example, a T-account for Cash shows all cash-related transactions, while the balance sheet reports the final cash balance alongside other accounts. The balance sheet is formal and used for external reporting, whereas T-accounts are internal tools for analysis.

T-account vs. Ledger

A general ledger is the master record of all accounts, containing every transaction a company records. T-accounts are a simplified version that focuses on one account at a time. The ledger is comprehensive but complex, while T-accounts are user-friendly for analyzing specific accounts.

For instance, a ledger might list thousands of transactions across all accounts, but a T-account for accounts receivable isolates just that account’s activity. Accountants often use T-accounts to double-check ledger entries or spot errors.

T-account vs. Trial Balance

A trial balance lists all account balances at a specific point to ensure that debits equal credits. T-accounts contribute to the trial balance by providing the raw data for each account’s balance. However, a trial balance is a summary, while T-accounts show the detailed transaction history.

If a trial balance doesn’t balance, accountants use T-accounts to trace errors back to specific transactions. T-accounts are a troubleshooting tool, while the trial balance is a checkpoint.

Wrapping Up

Ultimately, T-accounts offer a simple yet powerful way to understand financial flows and catch errors early. Due to their limitations, they cannot replace complete accounting systems, but they remain vital for small businesses. Larger organizations rely on them for troubleshooting rather than primary record-keeping.

After all, when combined with accounting software, T-accounts provide continuous and precise support that ensures clear and effective financial management.

")